Academy Bank

1201 Walnut St Kansas City MO 64106

What can we help you find?

Contact Us

Bank Routing Number

107001481

Bank by Mail/General Mail

PO Box 26458

Kansas City, MO 64196

Deposit Only Mailbox

PO Box 26744

Kansas City, MO 64196

Phone Number

1-877-712-2265

Download our app

Access your

accounts here.

accounts here.

Grab your phone and scan the code to download!

not featured

2026-05-07

Home Mortgage

published

5-minute

Understanding Loan-to-Value (LTV) Ratio & How to Calculate It

-

-

When you apply for a mortgage (or any loan secured by something valuable), lenders look at more than the dollar amount you are requesting. They also want to understand how much of the property’s value they would be lending to you.

This relationship is called the loan-to-value ratio, or LTV, and it plays a major role in how lenders evaluate your application and what terms they offer.

Key Takeaways: LTV Explained

- LTV stands for loan-to-value ratio—a percentage that determines how much of a property’s value is financed by a loan.

- A lower LTV generally means less risk for the lender, which can translate to better loan terms for the borrower.

- LTV is used across mortgage loans, HELOCs, auto loans, and refinances.

- An LTV above 80% on a conventional mortgage typically triggers the requirement for private mortgage insurance (PMI).

- Combined loan-to-value, also known as CLTV, accounts for multiple loans that are tied to the same asset or property.

What is Loan-to-Value Ratio?

Loan-to-value ratio, or LTV, is a percentage that expresses how much of a property's value is being funded by debt (like loans or lines of credit).

In mortgage lending, LTV compares the loan amount to the appraised value of the home. In auto lending, it compares the loan amount to the vehicle's value.

The same concept applies across most secured loans. Any time a loan is tied to an asset, lenders use LTV to help assess risk.

A lower LTV means you have more ownership of the property compared to what you still owe. A higher LTV means you have less ownership and more debt, which can make you a riskier borrower.

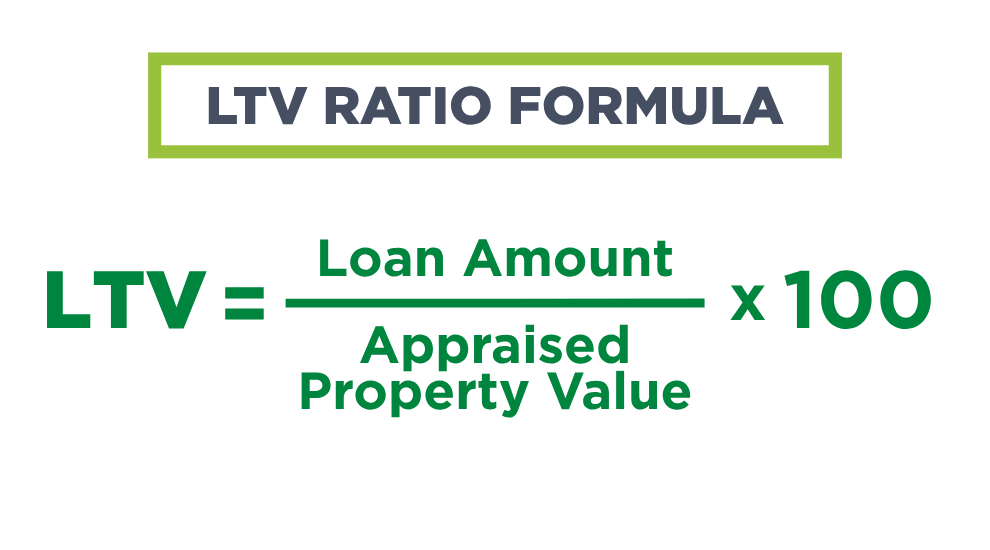

How to Calculate LTV

The LTV formula is fairly simple to calculate: LTV = (Loan Amount ÷ Appraised Value) x 100

Example: Calculating LTV on a Home Purchase

Let’s say you are buying a home appraised for $300,000, and you are making a down payment of $60,000. That means you are borrowing $240,000.

- STEP 1: Identify your loan amount.

$300,000 - $60,000 = $240,000

- STEP 2: Divide the loan amount by the appraised value.

$240,000 ÷ $300,000 = 0.80

- STEP 3: Multiply by 100 to express as a percentage.

0.80 x 100 = 80% LTV

What is a Good LTV Ratio?

For conventional mortgages, an 80% LTV (or lower) is generally considered ideal. Why? With an LTV of 80% or lower, borrowers can typically bypass the requirement for private mortgage insurance (PMI). PMI is an extra monthly cost that protects the lender in case the borrower is unable to repay their loan.

Above 80% LTV, most conventional lenders require PMI until the loan balance drops to that threshold. This is why the down payment decision is so important: Putting down enough for an 80% or lower LTV can greatly reduce the ongoing cost of the loan.

That said, "good" LTV depends on the loan type. FHA loans (Federal Housing Administration loans), for example, let you buy a home with a higher LTV and lower down payment, but they require mortgage insurance costs.

The right LTV target depends on your loan program and your overall financial situation.

How LTV Affects Your Mortgage Interest Rate?

LTV doesn't just determine whether PMI applies—it also influences the interest rate offered by lenders. Borrowers with lower LTV ratios are generally seen as less risky, which can result in better mortgage rates.

The relationship isn't always dramatic at every tier, but as LTV climbs higher above 80%, the rate offered may reflect that increased risk. Over the life of a 30-year mortgage, even a slightly higher rate can mean paying thousands more in interest.

This is why making a larger down payment can reduce the long-term cost of your mortgage, even beyond avoiding PMI.

LTV in Real Estate and Refinancing

LTV doesn’t just matter when you buy, it also matters when you refinance. If your home’s value has increased since purchasing, your LTV may be lower. This can happen even if your loan balance hasn't changed dramatically.

Going back to our example: When you originally borrowed $240,000 for a home that’s worth $300,000, your LTV was 80%.

A few years later, that same home is appraised at $350,000. Your LTV on the $240,000 loan drops to about 69%. That improved ratio may open the door to better refinancing terms.

LTV also matters with a cash-out refinance, where the new loan amount is higher than the existing balance. Lenders typically set a maximum LTV of 80%, which limits how much equity you can access.

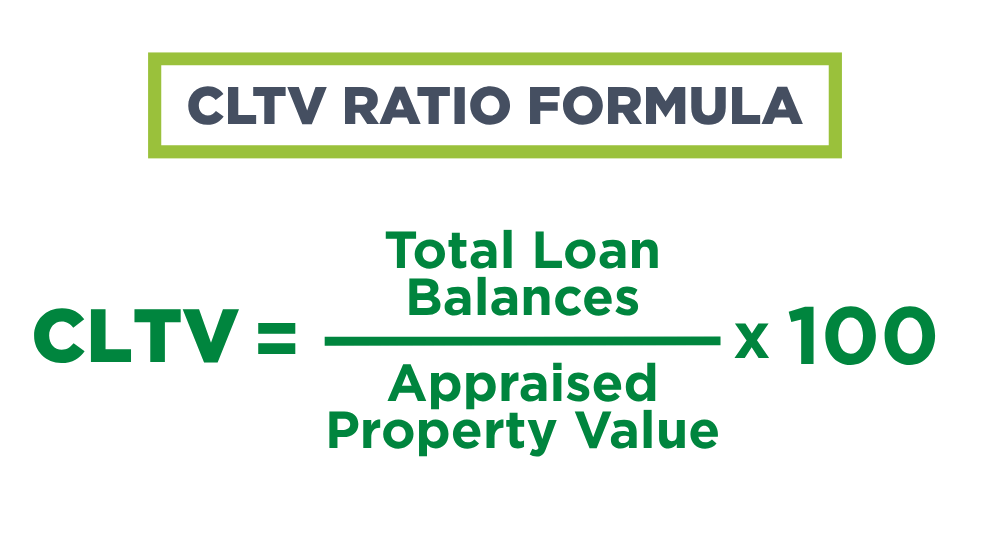

HELOC LTV and Combined Loan-to-Value (CLTV)

When more than one loan is secured by the same property, lenders use a related metric called “CLTV,” or combined loan-to-value ratio.

CLTV = (Total Loan Balances ÷ Appraised Value) x 100

CLTV most commonly applies to home equity lines of credit, or HELOCs. If you have a primary mortgage and you're applying for a HELOC, the lender will calculate CLTV by adding both balances together, then that total is compared to the home's value.

Most lenders set a maximum CLTV for HELOCs—typically around 85% according to Experian, though the number varies. Understanding CLTV is important when evaluating how much equity is actually accessible through a second loan or line of credit.

How LTV Works on Auto Loans?

Though the dynamics are slightly different, LTV applies to vehicle financing as well. Because cars depreciate (often quickly in the first few years), auto loan LTV can shift faster than it does with real estate.

An LTV above 100% on an auto loan means the loan balance exceeds the vehicle's current value. This is sometimes called being “underwater.” It can become a complication if the vehicle is totaled or if the borrower needs to sell the car before the loan is paid off.

How Do LTV and DTI Compare?

LTV and DTI (debt-to-income ratio) are both used in mortgage underwriting, but they measure different things.

- LTV shows how the loan amount compares to the home’s value.

- DTI shows how much of your income goes toward debt each month.

Lenders use BOTH formulas together to better understand the risk of lending to a borrower. A strong LTV with a high DTI—or vice versa—can affect approval and terms in different ways.

Choose Academy Bank for Home Loans and HELOCs

Whether you are buying a home, refinancing, or exploring a HELOC, understanding your LTV is a useful starting point. It influences your loan options, potential interest rates, and how much equity you can borrow.

Frequently Asked Questions: Loan-to-Value Ratio

What does LTV stand for?

LTV stands for loan-to-value ratio. It is a percentage that expresses how much of an asset’s appraised value is financed by a loan.

How is LTV calculated?

Divide the loan amount by the appraised value of the asset, then multiply by 100. For example, a $240,000 loan on a $300,000 home produces an LTV of 80%.

What is a good LTV ratio for a mortgage?

80% is the widely used benchmark for conventional mortgages. At or below 80% LTV, borrowers typically avoid PMI. Lower LTV ratios may also qualify for better interest rates.

What is the difference between LTV and CLTV?

LTV measures a single loan against a property’s value. CLTV—combined loan-to-value—adds together all loans secured by the same property. CLTV is commonly used when evaluating HELOCs or second mortgages.

How does LTV affect my mortgage interest rate?

Lenders generally offer more favorable rates to borrowers with lower LTV ratios, since less of the asset's value is financed through debt. Higher LTV ratios represent more risk for the lender, which can lead to a higher interest rate.

What is HELOC LTV?

For a HELOC, lenders typically look at CLTV, which is the combined balance of your primary mortgage added to the new HELOC amount you are requesting—all compared to your home's appraised value. Most lenders set a maximum CLTV for home equity lines of credit, often around 85%.

Does LTV apply to auto loans?

Yes. Auto loan LTV compares the loan balance to the vehicle's value. Because vehicles lose value over time, auto loan LTV can shift more quickly than it does with real estate.

What is PMI and when does it apply?

PMI stands for private mortgage insurance. On conventional loans, PMI is typically required when the LTV exceeds 80%. It protects the lender—not the borrower—and is usually removed once the loan balance drops to 80% of the home's value.

All loans and lines of credit are subject to credit approval. Terms, conditions, and loan program eligibility apply. Fees apply.