Academy Bank

1201 Walnut St Kansas City MO 64106

What can we help you find?

Contact Us

Bank Routing Number

107001481

Bank by Mail/General Mail

PO Box 26458

Kansas City, MO 64196

Deposit Only Mailbox

PO Box 26744

Kansas City, MO 64196

Phone Number

1-877-712-2265

Download our app

Access your

accounts here.

accounts here.

Grab your phone and scan the code to download!

not featured

2026-04-03

Home Mortgage

published

3-minute

Mortgage Pre-Approvals: What You Need to Know

-

-

Buying a home is an exciting milestone, but the process can feel overwhelming—especially at the beginning. One way to streamline the experience is by getting pre-approved for a mortgage BEFORE you start house hunting.

Keep reading to learn more about mortgage pre-approvals. We will explain:

- What mortgage pre-approval means

- How mortgage pre-approval works

- The benefits of getting pre-approved

- How long pre-approval takes

- How to get started with pre-approval

What Does Mortgage Pre-Approval Mean?

A mortgage pre-approval is a written estimate from a lender showing how much money you are eligible to borrow for a home purchase. While it isn't considered a final loan approval, it is a strong indication of your borrowing power based on your financial information.

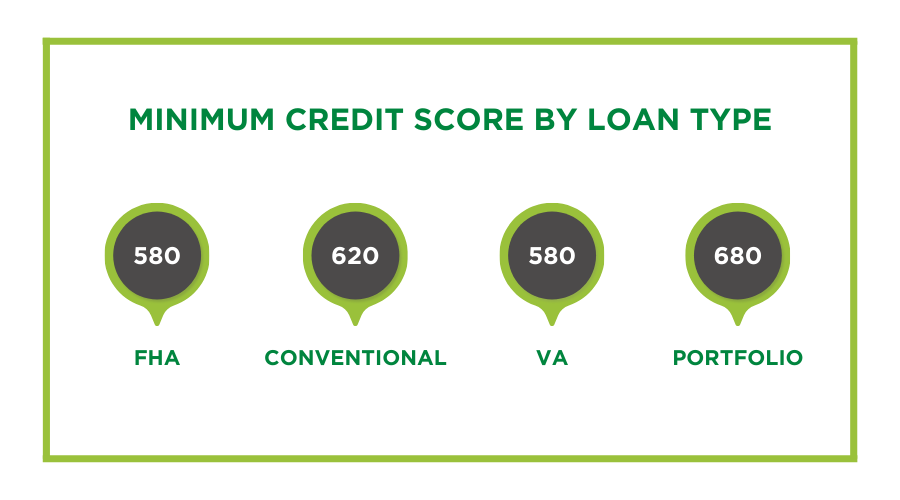

During the loan pre-approval process, mortgage lenders review key financial details, including:

- Income and employment history

- Credit score and credit report

- Debts and monthly obligations

- Assets like savings or investment accounts

This information helps the lender determine how much money you can comfortably afford to borrow and what loan terms apply.

How Does a Mortgage Pre-Approval Work?

To get the ball rolling on the mortgage pre-approval process, the prospective homebuyer—you—would fill out an application for a lender. This application will provide details about your income, assets, debts, and employment history.

The mortgage lender carefully examines your application and verifies your info with supporting documents (e.g., pay stubs, tax returns, and bank statements). This review gives the lender a better understanding of your financial health.

An important part of this process is the credit check, where the lender looks into your credit report and credit score. This assessment helps them decide if you are "creditworthy" (a reliable borrower) and the terms of pre-approval. Additionally, the lender usually considers other financial factors like debt-to-income ratio and job stability to gauge your capacity to handle a mortgage loan.

Once everything is reviewed, the lender approves or denies pre-approval. This gives you a clear picture of how much money you can borrow.

What are the Benefits of Getting Pre-Approved?

Getting pre-approved for a home loan offers several advantages that can make finding and buying a house much easier. Here are just a few of them.

BENEFIT #1: Know Your Homebuying Budget

By getting pre-approval, you will clearly understand how much money a lender is willing to finance. This information will help you narrow your home search down to properties within your price range. After all, you don't want to fall in love with a home that is too expensive!

Having a defined home budget upfront also helps you plan for other costs like taxes, insurance, and closing fees.

BENEFIT #2: Strengthen Your Offer with Negotiating Power

Sellers view pre-approval as a good sign. Why? Pre-approved homebuyers are seen as financially capable and worth considering. Sellers don't want to waste their time on buyers who aren't qualified or prepared.

In addition, having pre-approval gives you an edge in negotiations, helping you get the best terms.

BENEFIT #3: Speed Up the Mortgage Process

Once you find the right home, having your pre-approval in hand can shorten the time between your offer and closing. Since your financial information has already been reviewed, the mortgage lender moves faster through final underwriting and approval. This will help you get into your new home sooner!

BENEFIT #4: Spot Financial Issues Early

The pre-approval process reveals any potential obstacles that might affect your ability to qualify for a home loan. This usually includes high debt, inconsistent income, or credit issues. By identifying these early, you have time to address them and strengthen your financial profile, improving your overall loan options.

How to Get Pre-Approved for a Mortgage

Follow these steps to secure your mortgage pre-approval:

- Gather Documents: Be prepared to collect income statements, W-2 forms, recent tax returns, and bank statements.

- Compare the Best Mortgage Lenders: Look at rates, fees, and pre-approval offers from multiple lenders to find the right match.

- Submit Application: Complete the mortgage pre-approval application online or in person with your chosen lender.

- Undergo a Credit Check: Your lender will run a credit inquiry to confirm your credit score and history.

- Wait for a Decision: Most mortgage pre-approvals take anywhere from a few days to a week.

How Long Does Mortgage Pre-Approval Take?

The timeline for mortgage pre-approval can vary depending on your lender and how prepared you are with the required documentation. If your financial situation is straightforward and you provide the paperwork promptly, the process can be completed within a few days.

For more complex financial situations or if additional information is required, it may take up to a week or slightly longer. To keep the process moving quickly, it's important to stay organized and responsive!

How Long is Mortgage Pre-Approval Good For?

Most mortgage pre-approvals are valid for 60 to 90 days. In other words, they have a "shelf life." If you haven't found a home within that window, you may need to update your documents or reapply. Be sure to keep your financial information current and your credit stable during this time, which will streamline reapproval if needed.

Academy Bank: Your Mortgage Partner

Whether you are buying your first home or moving into your next one, Academy Bank is here to help! Our experienced loan advisors offer personalized guidance, competitive mortgage rates, and support every step of the way.

Ready to find your dream home? Explore our mortgage options and connect with a mortgage advisor to get started!

FAQ About Mortgage Pre-Approval

When should I get pre-approved for a mortgage?

It is smart to get pre-approved before you start looking at homes. Your pre-approval will show you exactly how much you can afford, and it will show sellers that you are a serious buyer. Most pre-approvals are valid for 60 to 90 days, so getting that approval early will give you plenty of time to find the right home before it expires.

Does getting pre-approved hurt my credit score?

Temporarily. A mortgage pre-approval requires a "hard credit inquiry," which can cause a small, temporary drop in your credit score (typically fewer than 5 points). This impact is minor, and your score will rebound quickly.

Pre-approval is a common and necessary step in getting a mortgage, so it's nothing to worry about.

Can I get pre-approved at multiple lenders?

Yes, you can apply for mortgage pre-approval with more than one lender to compare rates, loan terms, and fees. This will help you find the best deal for your budget.

IMPORTANT NOTE: Be sure to submit your applications within a short time frame—usually 14 to 45 days—so multiple credit checks count as just one inquiry on your credit report.

Can I get pre-approved if I'm self-employed?

Yes. Self-employed homebuyers can still get pre-approved for a mortgage, but lenders will look closely at the borrower's income stability. You will likely need to show two years of tax returns, profit-and-loss statements, and bank records.

What's the difference between getting pre-qualified and pre-approved for a mortgage?

Subject to credit approval. Each loan product listed has specific terms and conditions. Fees may apply.