Academy Bank

1201 Walnut St Kansas City MO 64106

What can we help you find?

Contact Us

Bank Routing Number

107001481

Bank by Mail/General Mail

PO Box 26458

Kansas City, MO 64196

Deposit Only Mailbox

PO Box 26744

Kansas City, MO 64196

Phone Number

1-877-712-2265

Download our app

Access your

accounts here.

accounts here.

Grab your phone and scan the code to download!

featured

2026-04-24

Financial Health

published

4-minute

Interest Paid Definition: What You Need to Know

-

-

When you take on debt, you don’t just pay back the amount you borrow. It also includes interest paid—the extra amount that you owe the lender on top of the original balance. Understanding how interest works can change the way you think about every loan, credit card, and mortgage you carry.

Whether you want to learn how interest is calculated, what drives your rate up or down, or how to reduce your total interest costs, this guide has everything you need to know. Let’s get started!

Key Takeaways on Interest Paid

- Interest paid is the cost of borrowing money, expressed as a percentage of the amount you owe.

- Different types of debt—mortgages, credit cards, auto loans, personal loans—each carry their own interest structures.

- APR reflects the true annual cost of borrowing (including fees), and it is the most useful number for comparing loans.

- How much interest you pay depends on your rate, your balance, and how long you take to pay it off.

- There are practical strategies to reduce the total interest you pay—and in some cases, the interest you pay may be tax deductible.

Interest Paid Definition

Interest paid is the amount of money a borrower pays a lender in exchange for accessing their funds. When a bank or lender extends credit—whether through a mortgage, a car loan, a personal loan, or a credit card—they charge interest as the price of lending money.

Think of it as the opposite of interest earned. When you save money in a bank account, the bank pays you interest. When you borrow money from a bank, you pay the bank interest. The same basic principle applies in both directions.

Interest is typically expressed as an annual percentage of the amount you owe, and it accrues over time until the balance is paid in full.

Principal vs. Interest: What's the Difference?

Before going further, it helps to understand the relationship between principal and interest—because every loan payment you make is divided between the two.

Your principal is the original amount you borrowed. Your interest is the cost layered on top of it.

Early in a loan's life, a larger portion of each payment typically goes toward interest. As the balance decreases over time, more of each payment shifts toward the principal. This is called amortization, and it's why paying off a loan faster can reduce the total interest you pay.

APR vs. Interest Rate: Which Number Matters?

When comparing borrowing options, you will come across two numbers that are easy to confuse: the interest rate and APR.

The interest rate is the base cost of borrowing, expressed as a percentage of the loan balance.

The APR (Annual Percentage Rate) is the broader number. It includes the interest rate PLUS any additional fees and costs associated with the loan, expressed as an annual rate.

For most borrowers, APR is more useful when comparing rates because it reflects the true cost of borrowing—not just the rate in isolation. Two loans with the same interest rate can carry very different APRs depending on fees.

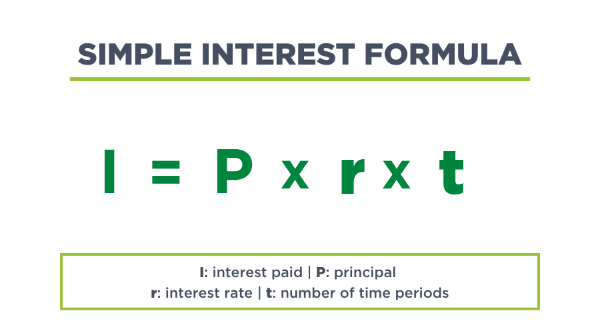

How is Interest Paid Calculated?

The math behind interest varies by loan type, but the foundational formula for simple interest looks like this:

Interest = Principal x Rate x Time

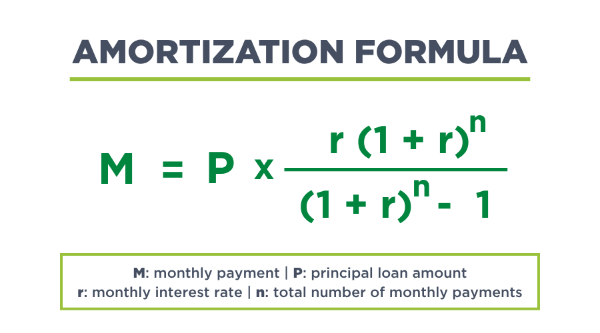

For most installment loans—like mortgages and auto loans—lenders use an amortization schedule that breaks each payment into principal and interest over the life of the loan.

Example: How to Calculate Interest Paid on a Loan

Let's say you take out a $20,000 auto loan at a 6% annual interest rate over 48 months.

- STEP 1: Convert the annual rate to a monthly rate.

6% ÷ 12 = 0.50% monthly rate, or 0.005 as a decimal

- STEP 2: Calculate your monthly payment using the amortization formula.

In the case of our example:

Principal (P) = $20,000

Rate (r) = 0.005

Number of months (n) = 48

Monthly Payment ≈ $469.70

- STEP 3: Calculate total amount paid over the life of the loan.

$469.70 x 48 = $22,545.60

- STEP 4: Subtract the original principal to find total interest paid.

$22,545.60 - $20,000 = $2,545.60 in total interest paid

With these examples, you can see why the loan term length matters so much. If you took out the same $20,000 loan at the same 6% interest rate (0.06) but paid it off over 60 months instead of 48, your monthly payment would be smaller (about $386)—but the total interest paid would be higher (about $3,199).

Types of Interest: Fixed vs. Variable

Not all interest works the same way. The two most common structures are fixed and variable rates.

A fixed interest rate stays the same for the life of the loan. Your payment is predictable, and the total interest you will pay is clear from the start. Fixed rates are common on mortgages, personal loans, and auto loans.

A variable interest rate can change over time, typically tied to a broader market index. Variable rates may start lower than fixed rates, but they carry more uncertainty. HELOCs and some credit cards carry variable rates.

Interest Paid by Loan Type

Differing lending solutions charge interest in different ways. Learn how interest paid works across some of the most common loan types:

Mortgage Interest

A mortgage is typically the largest type of loan most people have, and mortgage interest reflects that scale. On a 30-year mortgage, a significant portion of your early payments goes toward paying interest rather than principal. Over the life of the loan, total interest paid can rival—or even exceed—the original purchase price depending on the rate and term.

Mortgage interest is also one of the few areas where the IRS allows a deduction. Homeowners who itemize deductions may be able to deduct the mortgage interest they pay each year, which can reduce their taxable income. A tax professional can help determine whether this applies to your situation.

Credit Card Interest

Credit card interest works differently than installment loans. Instead of a fixed payment schedule, credit cards use a revolving balance—and interest accrues on whatever balance you carry from month to month.

Credit card APRs tend to be significantly higher than other forms of borrowing, which means carrying a balance can become very expensive. Paying the full balance each month is the most straightforward way to avoid paying credit card interest at all.

Auto Loan Interest

Auto loans are installment loans with fixed terms, typically ranging from 36 to 72 months. Interest is front-loaded through amortization, meaning a larger share of your early payments covers interest costs. Choosing a shorter loan term generally reduces total interest paid, even if the monthly payment is higher.

Personal Loan Interest

Personal loans typically carry fixed rates and fixed repayment terms. These are commonly used for debt consolidation, large purchases, or unexpected expenses. Because personal loan rates vary widely based on creditworthiness, your credit profile plays a significant role in how much interest you will pay.

HELOC Interest

A home equity line of credit (HELOC) allows homeowners to borrow against the equity in their home, usually at a variable rate. Interest is only charged on the amount drawn, not the full credit limit. HELOCs are often used for home improvements, large expenses, or consolidating higher-interest debt.

How to Reduce the Interest You Pay

Paying interest is part of borrowing—but how much you pay over time isn't necessarily a fixed amount. Here are a few ways you can reduce the total interest paid:

- Make extra payments toward the principal: Any payment above the minimum goes directly toward lowering your balance, which reduces the amount used to calculate future interest. Even occasional extra payments can help shorten your loan term and reduce the total interest you pay.

- Choose a shorter loan term when possible: A shorter term means higher monthly payments, but significantly less interest paid over the life of the loan. On a mortgage especially, the difference between a 15-year and 30-year term can result in tens of thousands of dollars in interest savings.

- Improve your credit profile before borrowing: Lenders use your credit score to determine your interest rate. A stronger credit profile generally earns a lower rate, and a lower rate means less interest paid from the very beginning.

- Consider refinancing if rates have dropped: If interest rates have fallen since you took out a loan, or if your credit score has improved significantly, refinancing may allow you to replace your current loan with a new one at a lower rate. That can reduce both your monthly payment and the total interest you pay over time.

- Pay credit card balances in full each month: Since credit cards carry some of the highest interest rates of any borrowing type, eliminating the balance each month is one of the most effective ways to reduce interest paid across your overall financial picture.

Is Interest Paid Tax Deductible?

In some cases, interest paid can be tax deductible, but it depends on the type of interest and your tax situation.

Mortgage interest is the most widely known tax deduction. Homeowners who itemize may be able to deduct interest paid on a primary or secondary residence, subject to certain limits.

Student loan interest may also be deductible, depending on your income and filing status.

Business loan interest is generally deductible as a business expense for qualifying businesses.

Credit card and personal loan interest paid for personal expenses is typically not deductible.

Tax rules change, and individual situations vary. For more guidance on your specific situation, it’s best to consult with a tax professional.

Interest Accrued vs. Interest Paid: Is There a Difference?

These two terms are related but not identical.

Interest accrued is interest that has accumulated on a balance but hasn't been paid yet. It continues to build until you make a payment. Interest paid is the amount that has actually been paid to the lender.

The distinction matters most in situations where interest accrues before payments begin, like during a deferment period on a student loan. It also matters if you miss a payment and interest continues to accumulate on your unpaid balance.

Find the Right Borrowing Option at Academy Bank

Understanding how interest works puts you in a better position to borrow wisely, whether you're considering a mortgage, a personal loan, or something else. The goal isn't to completely avoid borrowing altogether—it’s to choose a borrowing option that fits your budget and keeps your costs low.

Academy Bank offers a range of lending options designed to give you straightforward terms and competitive rates. Visit us online or stop by your local Academy Bank branch to talk through your borrowing needs with a banker.

Frequently Asked Questions: Interest Paid

What is interest paid?

Interest paid is the amount a borrower pays to a lender in exchange for using their money. It is calculated as a percentage of the outstanding balance and accrues over the life of the loan.

What is the difference between interest rate and APR?

The interest rate is the base cost of borrowing. APR (Annual Percentage Rate) includes the interest rate plus additional fees and costs, making it a more complete picture of what borrowing really costs.

How do you calculate interest paid?

Most loans use an amortization schedule that divides each payment between principal and interest. Early payments are weighted more heavily toward interest, with the balance shifting toward principal over time.

To make things easier, use a Loan Amortization Calculator.

What types of loans charge interest?

Mortgages, auto loans, personal loans, credit cards, student loans, HELOCs, and business loans all involve interest. The rate and structure varies by loan type and lender.

Can I reduce how much interest I pay?

Yes. Common approaches include making extra principal payments, choosing a shorter loan term, improving your credit score before borrowing, and refinancing when rates (or your credit profile) have improved.

Is loan interest tax deductible?

It depends on the type of interest and your situation. Mortgage interest and student loan interest may be deductible for qualifying borrowers. Credit card and personal loan interest on personal expenses typically is not. A tax professional can help clarify what applies to your situation.

What is the difference between fixed and variable interest?

A fixed rate stays the same for the life of the loan. A variable rate can change over time based on market conditions, which affects both your payment and the total interest you pay.

All loans and lines of credit are subject to credit approval. Terms, conditions, and loan program eligibility apply. Fees apply.