Academy Bank

1201 Walnut St Kansas City MO 64106

What can we help you find?

Contact Us

Bank Routing Number

107001481

Bank by Mail/General Mail

PO Box 26458

Kansas City, MO 64196

Deposit Only Mailbox

PO Box 26744

Kansas City, MO 64196

Phone Number

1-877-712-2265

Download our app

Access your

accounts here.

accounts here.

Grab your phone and scan the code to download!

featured

2024-03-21

Credit

published

Credit Scoring: What Factors Affect Your Credit Score?

-

-

Welcome to the world of credit scores, where three digits can hold a significant influence over our financial lives. In simple terms, a credit score is like a report card for our finances. It crunches our borrowing history, payment habits, and overall reliability into a single number, giving a snapshot of our financial health and behavior. But a good credit score is more than just a number—it opens doors to financial opportunities and may offer you access to better interest rates, loan terms, employment prospects, and more.

Today, we're getting straight to the point by breaking down the key factors in credit scoring. We'll explore the main elements that determine your creditworthiness, while also touching on effective credit building tactics like secured credit cards. Let's dive into the specifics and uncover what truly impacts your credit score.

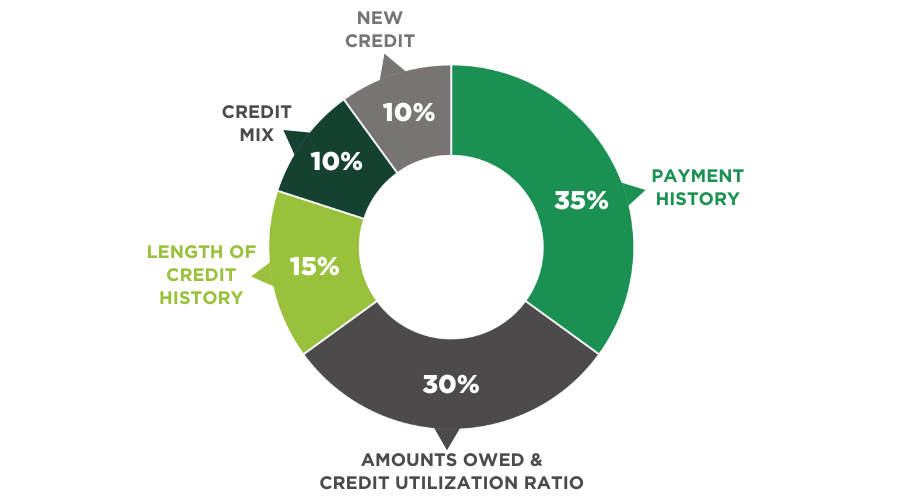

1. Payment History — 35% of Your Credit Score

Your payment history is the most influential factor in determining your credit score, accounting for 35% of the total. Consistently making your payments on time is crucial for establishing a positive payment history. This demonstrates to lenders that you’re reliable with credit, which is essential for maintaining a healthy credit profile.

2. Amounts Owed & Credit Utilization Ratio — 30%

The amount you owe and your credit utilization ratio are major factors that affect your credit score. This encompasses both the total amount you have borrowed and the percentage of your available credit currently in use. Furthermore, your spending behavior greatly impacts your credit utilization ratio and by extension, your creditworthiness.

Typically, individuals with high credit scores maintain utilization rates below 10% because higher ratios can negatively impact scores. Calculated as (Credit Card Balance / Credit Limit) x 100, this ratio constitutes about 30% of your FICO score.

3. Credit History — 15%

Your length of credit history, which is different from your payment history, reflects how long you've had active accounts. Generally, the longer your credit history, the better your credit score, and the average age of your accounts is also a factor. Lenders see a longer history as proof of your experience with handling credit responsibly. Credit history makes up about 15% of your FICO Score.

4. Credit Mix — 10%

Credit mix refers to the variety of credit types in your history, and this also affects your score. Lenders value seeing a mix of installment debt (like mortgages and student loans) and revolving accounts (like credit cards) as it shows your ability to manage various types of credit responsibly.

Having different types of loans and multiple open accounts shows lenders that you can handle different financial obligations effectively, making you a more attractive borrower. While it comprises about 10% of your FICO Score, a diverse credit mix with different types of accounts helps demonstrate your financial management skills and overall creditworthiness.

5. New Credit — 10%

When you apply for new credit, it can shake up your credit score, showing lenders how you handle borrowing and your potential risk. It's smart to avoid applying for multiple credit cards all at once since it makes you look less stable financially. That’s because statistics show that new debt increases the likelihood of falling behind on existing debts.

Plus, each credit card application triggers a “hard inquiry” into your credit score—which means a financial institution checks your credit. And during this process, your credit score is temporarily lowered. You can keep your credit profile healthy by being cautious, spacing out applications, and only applying when you really need to.

Building Credit with a Secured Credit Card

With a better understanding of credit scoring and how it works, it's time to put your knowledge into action and improve your financial standing. One of the best—yet often overlooked—strategies is building credit with a secured credit card.

A secured credit card functions much like a traditional credit card, but with one key difference: it requires a security deposit, which typically determines your credit limit. This deposit serves as collateral and minimizes risk for the lender, which is why secured credit cards are an accessible option for those with limited or poor credit history.

The beauty of a secured card lies in its ability to help you build credit responsibly. By using this card for everyday expenses and making timely payments, you can demonstrate trustworthiness to creditors.

At Academy Bank, we're proud to offer the Credit Builder Secured Visa® Credit Card, designed specifically to support your credit building journey. With features like automatic reporting to the three major credit bureaus, this card can help you strengthen your credit profile over time. Plus, you have the flexibility to set your own credit limit, ranging from $300 to $3,000, empowering you to manage your finances on your terms.

We are here to give you the tools and resources you need to succeed in your credit building journey. Our bank offers a suite of helpful resources, including a credit assessment calculator and a credit card payoff calculator, along with a wealth of valuable credit tips and advice.

With Academy Bank’s support paired with your commitment, it’s easy to pave the way for a brighter financial future. Take the first step towards stronger credit and greater financial freedom. We’re right here by your side.

Member FDIC

Subject to credit approval. Transaction and Penalty fees apply. Credit Builder Savings account required. $5.00 quarterly fee charged to the Credit Builder Savings account if not enrolled in eStatements. Improved credit score is not guaranteed. Credit score is determined by credit reporting agencies based on multiple factors, but satisfactory performance on a credit card product can improve your credit score. Default on a credit card, including missed or late payments can damage your credit score. Once added, funds cannot be withdrawn from the Credit Builder Savings account and the Credit Builder credit card without closing the savings account and the credit card.