Academy Bank

1201 Walnut St Kansas City MO 64106

What can we help you find?

Contact Us

Bank Routing Number

107001481

Bank by Mail/General Mail

PO Box 26458

Kansas City, MO 64196

Deposit Only Mailbox

PO Box 26744

Kansas City, MO 64196

Phone Number

1-877-712-2265

Download our app

Access your

accounts here.

accounts here.

Grab your phone and scan the code to download!

not featured

2020-11-24

Savings

published

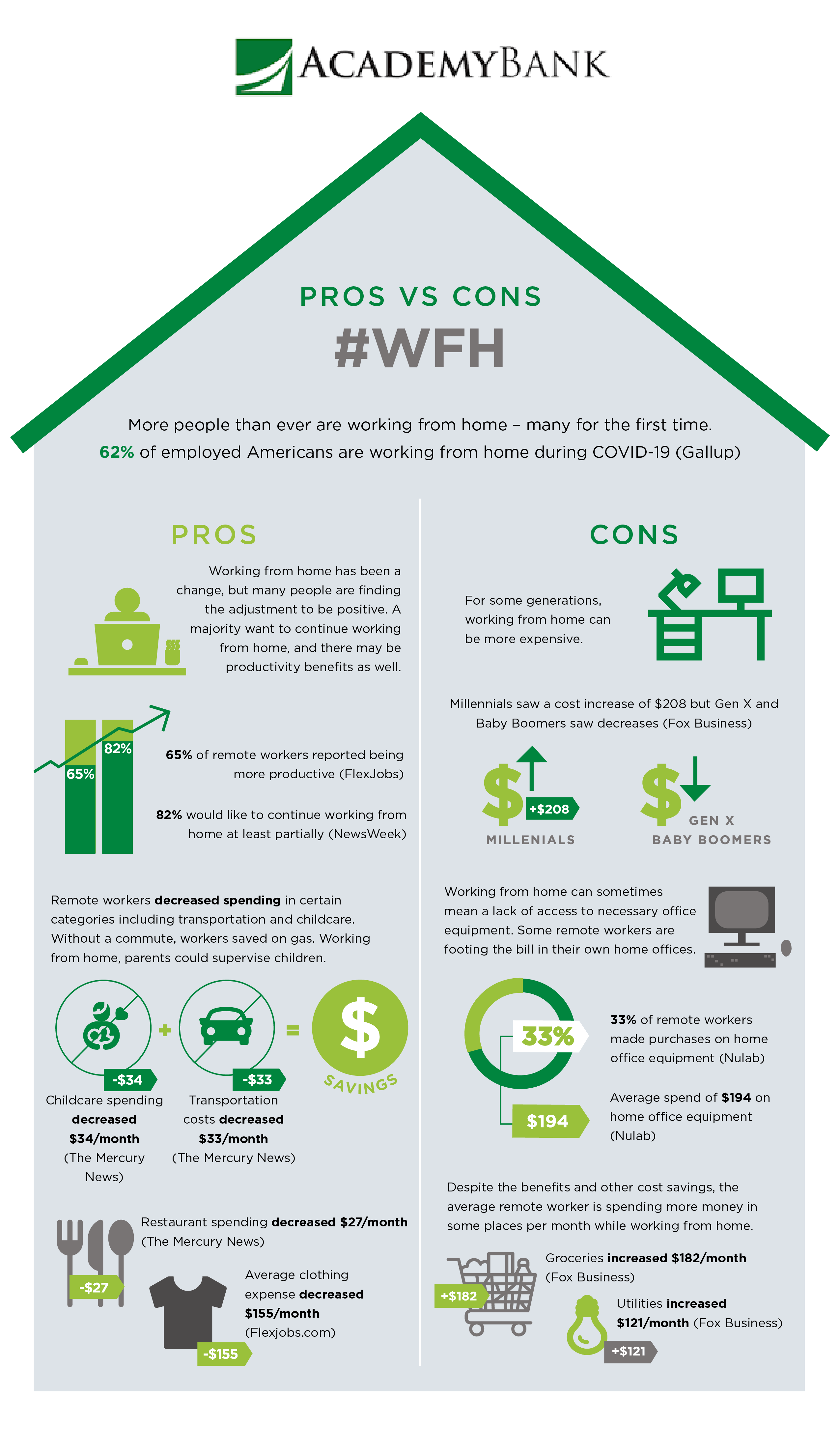

What are Financial Pros and Cons of Working from Home?

-

-

.png)

What are Financial Pros and Cons of Working from Home?

A year ago, there’s a good chance you weren’t working from home. But the international coronavirus (COVID-19) pandemic has changed everything -- in more ways than one. While previously, only 7% of Americans were able to work remotely, that number has skyrocketed in the past eight months as a result of the pandemic. But are there financial costs of working from home?

The answer, as with many things in life is: It depends. Sure, maybe you’ve cut out your commute. But are you spending more money on your electric bill in its place? Each person’s situation is unique, so the answer may be different for everyone. But several studies have aimed to take a look at the financial costs of working from home in general so we can get a sense of the trends.

Keep reading to find out more about the financial costs of working from home.

The Work-From-Home Experience

Before the pandemic, working remotely -- or telecommuting -- was a privilege that seemed reserved only for the select few. According to the 2019 National Compensation Survey (NCS) from the Federal Bureau of Labor Statistics, the 7% of people who could work remotely were more likely to be managers, other white-collar professionals, and those who are highly paid.

But as a result of COVID-19 and widespread mitigation efforts, including social and physical distancing, more workplaces have taken steps to limit in-person contact by urging or requiring employees to work from home. Which means many more people are working from home than ever before: by the end of June, that number had risen to 42%, according to research at Stanford.

As the pandemic stretches on, more people have settled into the routine of working remotely. When surveyed, 82% of remote workers said they’d like to continue working from home at least two days a week in the future, even after COVID-19 restrictions are lifted. Only 4% reported that they would not like to continue working from home at all -- not even once a week.

The disparities in opinion reflect the reality that everyone’s work-from-home experience can be vastly different and depend on a variety of factors. Whether it’s a lack of space for a home office or an unreliable internet provider, working from home can certainly impede productivity in some instances.

However, a study by FlexJobs shows that the majority of remote workers report being more productive while working at home compared to working in the office. 65% reported greater productivity, and 85% of businesses said productivity has increased due to greater flexibility.

The Hidden Costs of Working Remotely

While employees and businesses may benefit from a work and productivity perspective, the question still remains: how does remote work impact an employee’s finances?

To start with, many American workers needed to purchase their own equipment in order to work from home effectively. According to a study by collaboration software program Nulab, 33% of employees made purchases on home office equipment or office supplies. Of those who made purchases, the average spend was $194.

Remote workers also reported spending more money in a couple other areas that aren’t entirely surprising. The average grocery bill increased by $182 each month, which makes sense considering how much more time people are spending at home. And utilities increased by an average of $121 per month. With lights on and electronics plugged in all day rather than a few hours in the evening -- and using your own WiFi rather than the office network -- many Americans are facing higher utility bills than in pre-pandemic days.

You Spend Some, You Save Some

But it’s not all bad. Just as remote workers are spending more money in some areas, they’re also able to save money in some other areas. For example: the daily commute. Without the need to physically drive or take public transportation to the office, the average remote worker is saving $33 per month by working from home, cutting the commuting costs. And this doesn’t even factor in repair and maintenance costs, or the amount of time saved by eliminating that daily commute.

While grocery spending increased, restaurant spending decreased by $27 per month. Gone are the days (for now) of grabbing a bite at a nearby restaurant with co-workers because you didn’t feel like packing a lunch or were running short on time in the morning on the way out the door.

And parents are saving money in another category -- childcare costs. Although many parents are feeling the stress from being their kids’ homeschool teacher as well as keeping up with their full-time jobs, there’s one financial benefit. The average parent is saving $34 on childcare each month.

Interestingly, the change in money saved and spent as a result of working from home is not uniform across generations. For the three main generations currently in the workforce, the costs and benefits from working from home are drastically different. While Baby Boomers -- who have been working the longest and generally earn the most -- are able to decrease costs by $24 per month, Generation X is only saving about $2 per month. Millennials, on the other hand, are seeing their monthly expenses increase by an average of $208.

Your Personal Finance Partner No Matter What

As the uncertainty around the pandemic continues, we want you to know that Academy Bank is working hard to be your partner in personal finance. Whether you’re at home or in the office.

We want to help you keep your banking simple with our easy-to-use resources. So you can bank whenever you want, wherever you are.

Member FDIC